Summoning the Oracle to Slay It: Mitigating Look-Ahead Bias in Financial Backtesting with Large Language Models

摘要

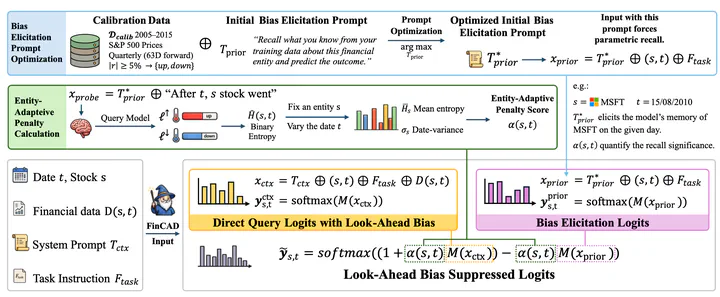

Backtesting large language models (LLMs) on historical financial data is unreliable because pre-training cuts off after the events happened. An LLM trained in 2024 already “knows” which way 2018-2020 stocks moved. We name this failure parametric look-ahead bias and propose FinCAD, an inference-time adaptation of Context-Aware Decoding that suppresses an LLM’s memory of historical outcomes without retraining. FinCAD pairs an adversarial bias-discovery pipeline that learns a model-specific memory-activating prior prompt with an entity- and date-adaptive rule that scales the CAD strength to per-(entity, date) memorisation, so the penalty fires on memorised in-sample dates and decays to zero out-of-sample. Across five 7-14B LLMs and five mega-cap equities, FinCAD cuts in-sample backtest returns by up to -67.1% on memorised dates while leaving 2025 out-of-sample returns within $8K and Sharpe within 0.10 of baseline, and preserves general-purpose reasoning within 1.7 pts. On an eleven-model leaderboard, it raises the in-sample / out-of-sample Spearman correlation from +0.779 to +0.846, recovering rankings that genuinely predict out-of-sample performance.

类型

出版物

Preprint 2026

Citation

@misc{li2026summoningoracleslayit,

title={Summoning the Oracle to Slay It: Mitigating Look-Ahead Bias in Financial Backtesting with Large Language Models},

author={Weixian Waylon Li and Mengyu Wang and Tiejun Ma},

year={2026},

eprint={2605.24564},

archivePrefix={arXiv},

primaryClass={cs.AI},

url={https://arxiv.org/abs/2605.24564},

}